End of the Texas Multifamily "Extend and Pretend" Era

🚨 The Texas multifamily "extend and pretend" era has officially ended. As we approach the May 5th foreclosure auctions, the data shows a harsh reality for over-leveraged sponsors—and a massive reset for the market.

At Kaliser & Associates, P.C., we are seeing a definitive shift in lender behavior, moving aggressively from loan modifications to active liquidations to clear out 2021-vintage bridge loans.

Here is what the numbers are telling us across the Texas Triangle heading into Q2:

🏙️ Houston (Harris County)

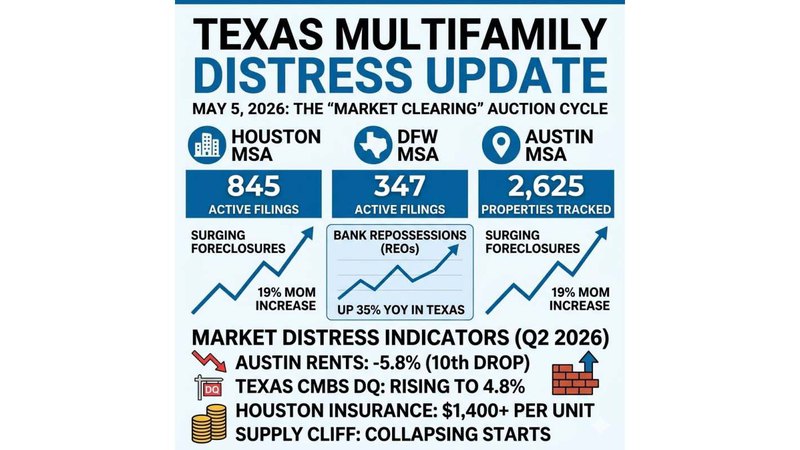

The state's undeniable epicenter for distress. Houston recorded 3,614 foreclosure starts in Q1, ranking second-highest in the U.S.

The local multifamily delinquency rate has spiked to 7.15%.

Distress remains heavily concentrated in Class B/C value-add portfolios.

🤠 Dallas-Fort Worth

347 filings in Dallas County during the latest cycle.

Despite strong absorption (over 25k units in the last year), the "maturity wall" is hitting syndicators who have exhausted all extension options on floating-rate debt.

🎸 Austin (Travis County)

Distressed property counts hit a seven-month high of 2,625 properties on April 27th (up 19.4% since September).

Austin currently leads the state in the pure velocity of new distress filings.

📉 The NOI Squeeze It is not just the debt yield causing pain; operational expenses are breaking pro-formas. We are seeing insurance premiums in Houston stabilize at a staggering $1,400+ per unit, pushing even fully stabilized, 90%-occupied properties into the red.

🌅 The Silver Lining If you look closely at the metrics—something we prioritize heavily through DynamicKpi.com—the approaching "Supply Cliff" is undeniable. Austin’s under-construction inventory has plummeted 73% from its peak. As new deliveries dry up in late 2026, demand is expected to finally outpace supply, which should compress the heavy 10-12 week rent concessions we are currently seeing.

The next 12 to 18 months will require sharp legal structuring, airtight operational processes, and highly disciplined capital. Institutional buyers are already catching the falling knives at 30% below developer basis.